Thank you for your decision to join the military and to serve our nation. Military life is a high calling, and while it's an exciting time, it can also be overwhelming.

When I left for basic training, I remember having a one-track mind with a singular goal: Learn what I needed to learn so I didn't get yelled at.

Now that I've retired from the military, I have the benefit of some wisdom that comes with hindsight. Read these 10 important steps as you begin your military career.

- Join USAA.

- Set up direct deposit.

- Draw up a will.

- Protect your life, loved ones and possessions.

- Create a budget.

- Save for emergencies.

- Take advantage of the Thrift Savings Plan.

- Purchase an affordable vehicle.

- Beware of predatory lenders.

- Save money through military discounts.

USAA was formed in 1922 when 25 Army officers met in San Antonio to mutually insure each other's vehicles. Obviously, I'm a bit biased, but I believe USAA membership is one of the most valuable benefits of military service.

That's because USAA serves military members during their time of service. And when their military service ends, the products USAA offers are theirs to keep and to pass down to family members. In fact, my kids were each about 2 weeks old when they became USAA members. Take your first steps to joining USAA today.

2. Set up direct deposit.

One of the first things you'll do as you join the military is set up direct deposit. This will be at the bank where you want your military paycheck to be deposited.

Be sure to choose a bank that fits your new military career. A USAA Classic Checking account is designed to match the military lifestyle. And, applying and opening an account is fast and easy.

3. Draw up a will.

Although you might not have much stuff now, you'll accumulate more over time. That's why a will is important: It lets everyone know what you want done with your possessions and money if you die.

The good news is that in the military, you can get a no-cost will through the Judge Advocate General, or JAG, office. JAG professionals are knowledgeable, helpful and a major benefit of military life.

4. Protect your life, loved ones and possessions.

As you join the military, make insurance a priority. Start by securing the following:

Life insurance

The military lifestyle is inherently dangerous. Servicemembers' Group Life Insurance, or SGLI, is a great benefit, and we strongly recommend taking advantage of it. However, SGLI may not be enough to meet your needs. Since you can’t take SGLI with you when you leave the military, you will eventually need your own life insurance policy. Not sure how much life insurance you need? Consider your family circumstances and financial goals to determine if SGLI is enough for you.

Renters insurance

If your items were destroyed in a fire today, do you have enough cash on hand to replace them? Most of us don't. Renters insurance can protect you from things like theft, flooding and even slip-and-fall accidents. Renters insurance can be especially important for members of the military.

When you have USAA’s renters insurance, you're covered at home, during PCS and deployment, and everywhere in between.

Auto Insurance

Getting a new, or new to you, car is exciting, but auto insurance? Not so much. Nevertheless, you need it because military installations and states require it. To make sure you are adequately covered, learn more about how to protect yourself with proper insurance coverage. Then, take steps to protect yourself by applying for auto insurance.

5. Create a budget.

When you join the military, it might be the first time you are earning a consistent paycheck. It's important to get the most out of what you earn, and that means creating a spending plan that gives each dollar a mission.

The mission of one dollar might be to pay for rent, another dollar might be to buy groceries, and another for entertainment. To make sure you know what each dollar's mission is, it's helpful to create a budget. This can also help you achieve the important financial goal of spending less than you earn.

One expense many people forget to budget is uniforms. If you're an officer, you'll need to budget for uniform purchases. If you're enlisted, you'll have a clothing allowance, but use it wisely so you can use your paycheck to fund other financial goals.

6. Save for emergencies.

In the military, emergencies will happen. Your car will break down unexpectedly. You'll need to fly back for a family member's funeral. Or the water heater in your home will need replacing. That's why it's important to build an emergency fund.

We recommend having three to six months of living expenses saved in an emergency fund. When you're just getting started in military life, that can feel like a large number. So, start with a smaller goal that you can reach in a shorter timeframe. It can serve as motivation while you work towards the bigger goal.

It will take time, but if you're disciplined in your saving habits, you can get there sooner than you think. Just make sure to set these funds aside in a dedicated savings account. That way, you don’t accidentally spend emergency fund money on pizza.

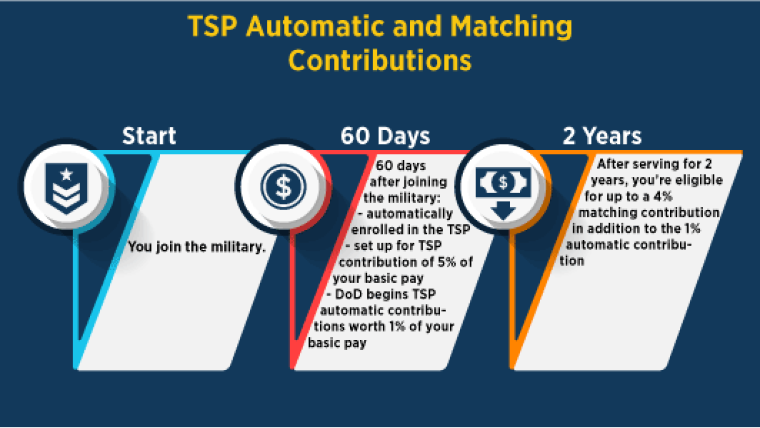

7. Take advantage of the Thrift Savings Plan.

One of the best ways to achieve your retirement goals is to save early and save often. The military's version of a 401(k) is the TSP or Thrift Savings Plan Opens in a New Window. See note 1

The graph below shows when you become eligible for the different aspects of the Blended Retirement System. We recommend contributing at least 10% of your pay toward retirement goals.