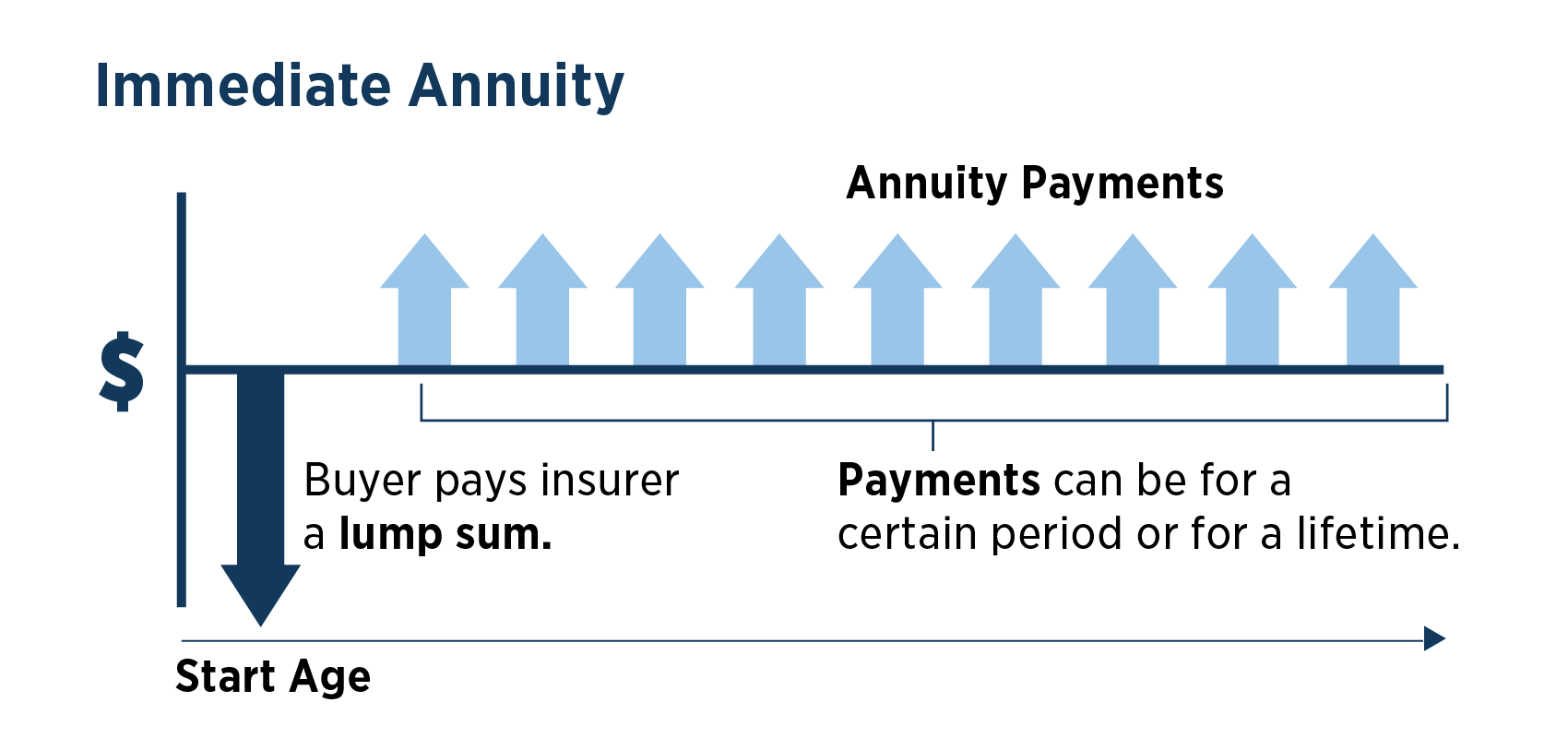

- A unique feature of immediate annuities is what's known as longevity crediting or mortality crediting. This feature allows the insurer to pay out a guaranteed benefit over a longer time period. With an immediate annuity, premiums paid by those who die earlier than expected contribute to gains for the group of immediate annuity contract owners. As a result, survivors in the group, known as a pool, receive a higher yield, or credit.

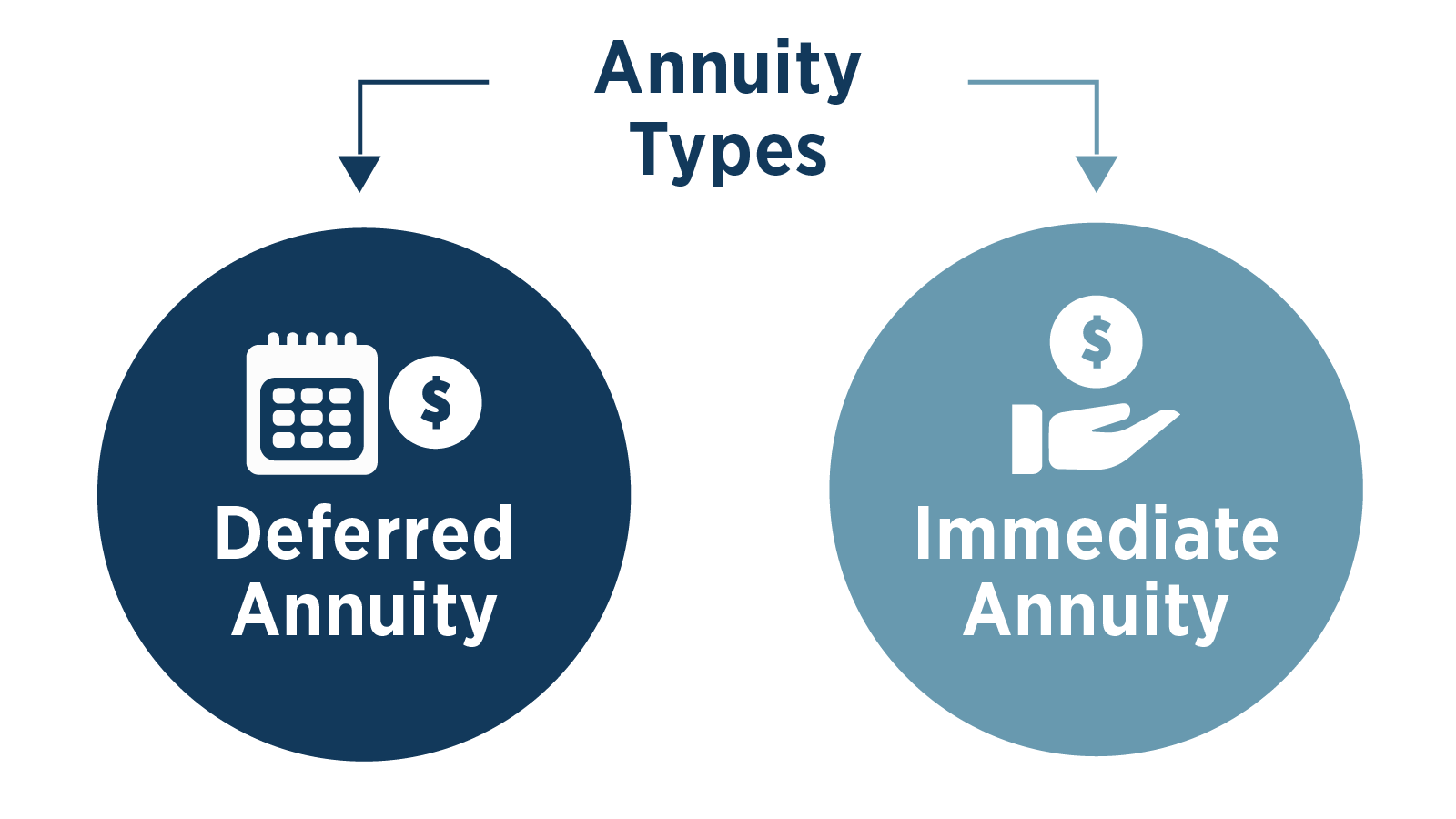

Although there are many types of immediate annuities available, here are two of the most common types that people ask about:

- Fixed immediate annuities have periodic payout amounts that stay the same, or are fixed, for life or a stated period. This type of annuity can be useful for those seeking safe, steady income, and who may have other resources to manage inflation.

- Variable immediate annuities start paying out right away, the same as a fixed immediate annuity. But unlike fixed immediate annuities, the periodic payment amount from a variable immediate annuity can fluctuate based on the underlying portfolio's performance. This kind of annuity might work best for those who want steady income but are willing (or who need) to take on a degree of risk with fluctuating payments.

How does an annuity work?

It's important to understand how annuities work when it comes to the accumulation versus payout (or annuitization) period, some tax considerations, and how minimum required distributions work with annuities.

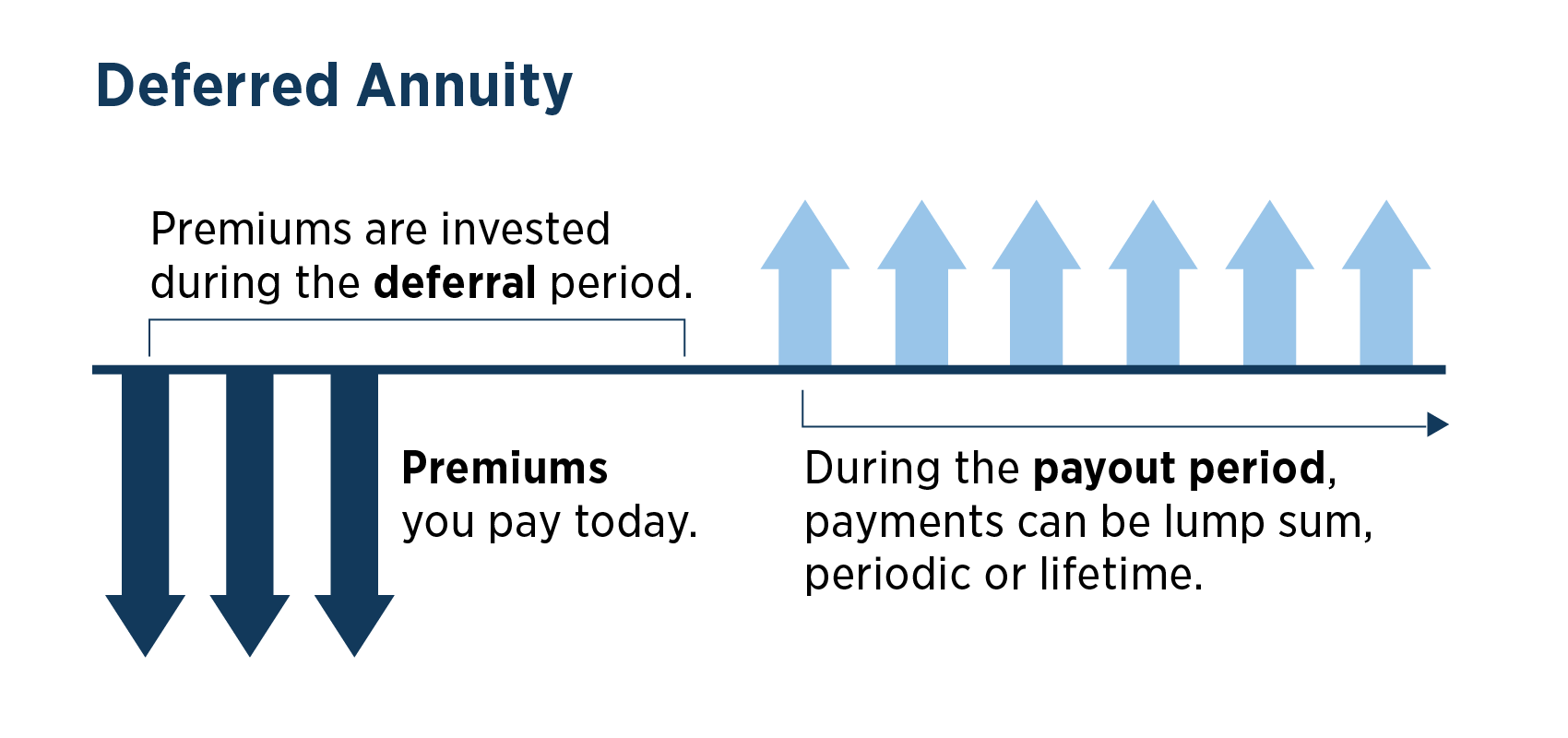

Accumulation period versus annuitization period

During the accumulation period, you put money into the deferred annuity to grow over time. When the money is needed later (usually for retirement), the annuity can pay out either a steady stream of income (annuitization) or variable sums.

Tax options for owning an annuity

Annuities can be owned inside or outside of an IRA or retirement account (qualified accounts). Deferred annuities grow on a tax-deferred basis. Withdrawals or income are taxed as ordinary income if held in a qualified account, tax-free if held in a Roth account or partially taxed if held in a nonqualified account. Immediate annuity income from a qualified account is fully taxable, tax-free if held in a Roth and partially taxed using what is called an exclusion ratio calculation if held in a nonqualified account. With most nonqualified annuities, the idea is for the owner to wait at least until age 59½ before making withdrawals without penalties or fees.

Annuity minimum distributions

If the annuity is held in a traditional IRA or retirement plan (qualified accounts), the IRS-required minimum distribution rules apply. For qualified accounts, the amount annuitized is considered by the IRS to have met the minimum distribution requirements. Although there are no minimum distribution requirements for nonqualified annuities, the earnings on the annuity are taxable as ordinary income.

What are the pros and cons of different annuities?

Think of an annuity as a tool in your tool chest. Each tool usually performs different functions, and some might be able to do more than one task. Still, just as it's hard to compare the pros and cons of a screwdriver versus a wrench, the same thing applies to annuities. Similarly, a $5 screwdriver may be all you need for a simple task, versus a $30 ratchet. As such, it's more important to consider the type of annuity best for you based on your needs and goals. The following can help point you in the right general direction.

Which type of annuity fits your needs and goals?

Consider the following two scenarios:

- Retirement is far away, but you want some guaranteed savings, OR

- Retirement is getting closer, and you will need some guaranteed income.

If you'll need the money in the future, then a deferred annuity may be appropriate. The following explains which might best fit your needs if you also want the following features or benefits:

- If you want a guaranteed rate of return, you may want to consider a deferred fixed annuity.

- If you want some potential for market gains, you may want to consider a deferred indexed annuity.

- If you want more potential for market gains, you may want to consider a deferred variable annuity.

- If you want more potential for market gains and an option that includes minimum income and withdrawal benefits, you may want to consider a deferred variable annuity with guarantees for minimum income or withdrawals.

- If you want guaranteed income starting much later, you may want to consider a deferred income annuity.

Now, consider this third scenario:

- You're retired and want or need guaranteed income now.

If you'll need the money now, an immediate annuity might be appropriate. The following explains which might best fit your needs if you also want the following features or benefits:

- If you want income for as long as you live, you may want to consider a life only immediate annuity.

- If you want income for a fixed period of time only, you may want to consider an immediate annuity with a period certain. You can also add a beneficiary who may continue getting paid if you die before the guaranteed period ends.

Note: You can combine the first two benefits to achieve income for life and a guaranteed period of time. You can also add a beneficiary who may continue getting paid if you die before the guaranteed period ends.

- If you want inflation protection, you may want to consider an immediate annuity with a future increase rider.

- If you want a return on your money if you die early, you may want to consider an immediate annuity with return of premium benefit.

What's the best age to get an annuity?

A lot of the decision-making boils down to your needs and goals (see previous), your age and your life expectancy. Consider the following:

- Deferred annuities could be a good choice when you have some time for accumulation, you want to dedicate a portion of your assets to a particular want or need, such as establishing a stable floor to generate retirement income, or you're seeking a degree of creditor protection.

- Immediate annuities might make sense if you need a stable source of retirement income or want to supplement other retirement income. Since immediate annuities include three payout components — return of principal, interest earned and longevity credits — the timing matters. You can think of longevity credits as the money unclaimed by those in the insurance pool who die early. Those who continue to live are the beneficiaries of these credits. Although it's complicated, the initial payout rate for immediate annuities is generally higher the older you are.

Annuities can play a role in an overall retirement strategy, during both the accumulation and income phases. Immediate annuities primarily support retirement income strategies, while deferred annuities may support growth, tax-deferral, legacy, and later-life income strategies. It's important to educate yourself about annuities before you make a decision (visit the FINRA websiteOpens in a New Window). See note 2 To learn more about annuities, call a Retirement Income Specialist.

Comparison of Features with Different Types of AnnuitiesOpens in a New Window

IMPORTANT: Annuity features, requirements and alternatives should be discussed with your financial advisor or qualified legal and tax counsel. Consider the following:

- Annuities may not be as liquid as other alternatives and usually requires a long-term time commitment.

- Initial sales charges, commission and ongoing fees can vary between types of annuities and providers.

- Annuities could be subject to surrender charges by the provider or IRS penalties for withdrawals before age 59½.

- Most annuities are backed by the ability of the provider to pay. Therefore, the financial strength of the provider is vitally important.

- Understand how annuities can be owned (usually must be a natural person).

- Consider estate planning and gifting considerations before purchasing an annuity.

- Consider the taxation of annuities upon distribution or for beneficiaries.

- Know the required minimum distribution (RMD) rules for qualified annuities and how they can affect your beneficiaries. The ability to aggregate RMD rules within a qualified annuity contract can vary among providers.

- Understand the different parties involved with an annuity: contract owners, annuitant and beneficiary.

- Consider how other fixed income financial solutions may serve as alternatives to annuities.