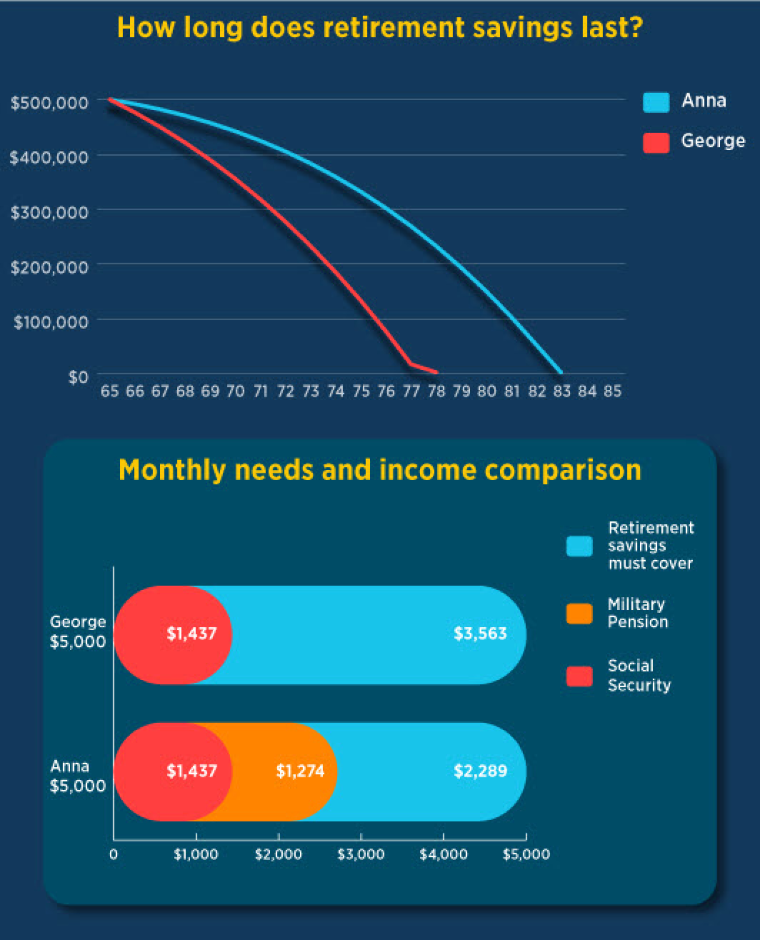

Consider this: There's another important takeaway from this analysis. Even with Social Security and military benefits, Anna will likely outlive her savings.

As you plan for retirement, think about how you want to live. As a general rule of thumb, you can expect your retirement expenses to be 70% to 85% of what they were in the final years of your career. If your retirement salary is $100,000 a year, you might expect for $70,000 or $85,000 of yearly retirement expenses.

Now add your expected military retirement and SSB. If that number falls short of your expenses, you'll want additional retirement savings.

Don't forget: If you chose Option A for your Reserve Component Survivor Benefit Plan (RCSBP), age 60 is when you'll make your RCSBP decision. If you have a family member who relies on your income, consider passing a portion of your military retirement pay on to them by electing RCSBP coverage. This helps provide for them financially in case you die. Learn more about your RCSBP decision.

Reason 2: You become eligible for TRICARE.

Health care costs rise as we age. TRICARE offers health care for military members and their families, including retired active-duty Reserve and Guard members. There are a lot of great reasons to sign up: Expenses are low, premiums are low and deductibles are low. Now, lower is a relative term but it is lower than many health care plans I've researched.

Consider this: Unfortunately, not all providers accept TRICARE. Rural areas may have a smaller number of doctors, which means you could have to travel some distance for your health care.

The bottom line is, before you decide on TRICARE for yourself and your family, check with your preferred providers to be sure they accept it.

Reason 3: At 65, you get TRICARE For life.

At this point, Medicare becomes your primary health insurance, and TRICARE For Life serves as a free supplement that covers additional costs. TRICARE For Life is free for those who are enrolled in Medicare Parts A and B and are paying their Medicare Part B premiums. If this is all confusing language, I suggest you read our article that gives a good overall summary of Medicare.

A recent study from Fidelity showed that a 65-year-old couple could pay $315,000 out of pocket for health care costs over the remainder of their lives. When you consider that the TRICARE For Life catastrophic cap is $3,000 per year, a person who lives to age 95 will pay a maximum of $90,000, far less than the $315,000 from the recent study.

Consider this: You may need to switch doctors if you switch to TRICARE. Be sure to shop around to be sure your medical needs will continue to be met. For more information, read the article How to get health insurance when leaving the military.

Military retirement and long-term planning

Depending on your individual situation — whether you're an active-duty retiree or retired from the National Guard or Reserves — benefits like TRICARE and military retirement can help safeguard your golden years.

Even if you're like me and 60 feels a long way off, just knowing military retirement and TRICARE are on their way can grant some peace of mind as you budget for retirement.

No matter where you are in your career or how long it is until you begin to receive your well-earned military benefits, it's never too late to make adjustments to ensure you have the income you need in retirement.