How are ETFs and mutual funds different?

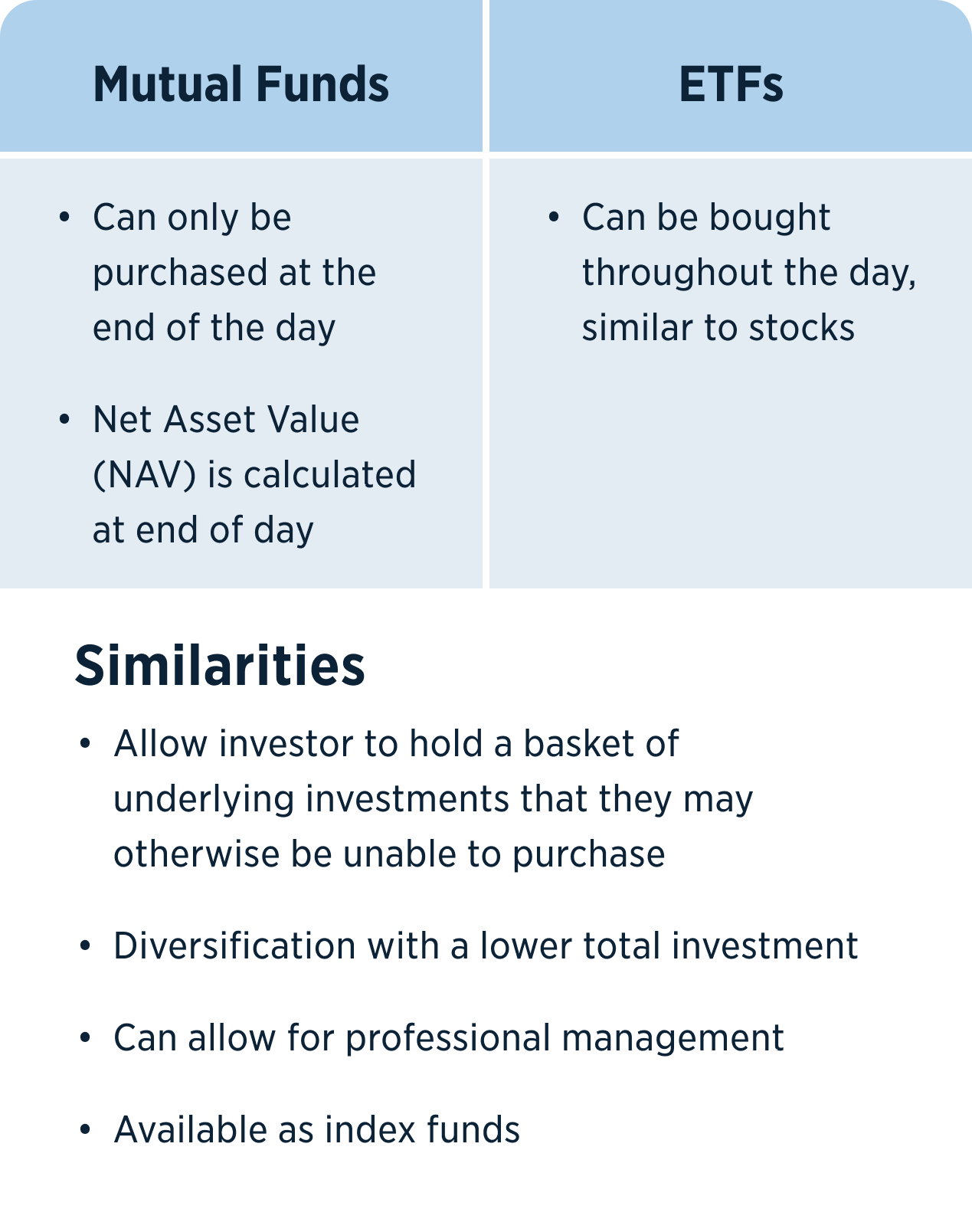

One of the big differences between ETFs and mutual funds is when they can be purchased. ETFs can be bought throughout the day, similar to stocks, whereas mutual fund transactions occur after the market closes when the mutual fund is priced.

To understand how that works, let's start by looking at how mutual funds are priced. At the end of each day, a mutual fund's Net Asset Value, or NAV, is calculated by taking the value of all its assets and dividing that by the number of outstanding shares.

For example, at market close, the value of the securities owned by the mutual fund is $100 million, and it has 5 million shares outstanding. If an investor purchases this mutual fund, they'd pay the NAV of $20 plus any purchasing costs.

Keeping with that same example, at the end of the second day, the value of the underlying security increases to $105 million and still has the same 5 million shares. Therefore, the NAV would increase to $21.

While a mutual fund sells at its NAV at the end of the day, an ETF can trade at a premium or discount during market trading hours.

Let's say the value of the underlying assets of an ETF puts its value at $20, but it's currently selling for $20.50 on an exchange. In this case, it's selling at a premium and, if you want that particular ETF, you have to pay more than it's worth. The exact opposite is referred to as "selling at a discount."

Types of ETFs and mutual funds

With so many different mutual funds and ETFs out there, most people have no trouble finding one that aligns to their goals. Here are some of the most common ones.

- Equity funds invest in U.S. funds, foreign funds or both. One example is a mutual fund that invests in small-cap, U.S. stocks.

- Fixed income funds are investments that provide income from assets such as bonds.

- Asset allocation funds usually contain a mix of asset classes. For example, the fund might have 75% in stocks, 15% in bonds and 10% in cash.

- Index funds are passively managed mutual funds that seek to track an index, like the S&P 500®. They own the stocks that make up that index and attempt to match index performance minus expenses. If a stock is removed from the index, the portfolio manager also removes that stock from their index fund.

- Target date funds automatically rebalance to reach a target risk tolerance by a selected date. For example, let's say you plan to retire in 2060. As that year approaches, the fund becomes more conservative by selling stocks and purchasing bonds or increasing cash allocation.

- Money market funds usually invest in lower-risk investments, such as U.S. treasures, to return a small income.

- Environment social and governance funds are socially responsible funds that avoid particular sectors or stocks based on environmental, human rights or religious preferences.

How mutual funds and ETFs are managed

Both mutual funds and ETFs can be actively or passively managed. Here's the difference:

- In the case of actively managed ETFs and mutual funds, the professional portfolio manager tries to "buy low and sell high" to outperform a benchmark, or the market as a whole. Because of fees, an actively managed mutual fund needs to beat its benchmark just to break even. For example, if a mutual fund has a 1% expense ratio and the market return is 6% this year, the mutual fund needs to return 7% just to match market return.

- In the case of a passively managed fund, the goal is to match the performance of an index, minus fees.

At this point, a reasonable investor might ask: Why not choose an investment that is at least trying to outperform the market?

During times of market corrections over the past 35 years, active management outperformed passive management 18-17, according to a 2022 Hartford Funds study Opens in a New Window. See note 1 That's close enough, even for me.

Investopedia gives another look at active versus passive management in their article The Low Down on Index Funds Opens in a New Window. See note 1 Their takeaway: Over the short term, some actively managed mutual funds can outperform the market. But over the long term, active management tends to underperform passive investing.

It all comes down to the strength of the portfolio manager, the person doing the research and making the buy and sell decision. How good are they at identifying underpriced or undervalued stocks? Can they find those securities that will outperform the market, even when considering fees and taxes? Sometimes yes, sometimes no. Even Babe Ruth, as exhilarating as his home runs were, struck out more times than he knocked it out of the park.

Because even the savviest professional isn't error-proof, it's important for investors to do their research.

Risks of investing

Whether you purchase a mutual fund or an ETF, investing carries risk. In my opinion, one of the most dangerous statements is: "This company has been around for 100 years; it's a safe bet."

In truth, you never know what the future holds — for the company and for the sector. Camera film stocks performed well for years, but you can imagine how they've done since the advent of the smart phone.

Even if a single company or sector continues to perform well, global risks are nearly impossible to predict. The S&P 500® reached its peak on February 19, 2020 before it plummeted 66% over the next 24 days as COVID-19 reached pandemic status.

Because markets by nature go up and down, it's important to invest according to your risk tolerance and risk capacity. One key part of this decision is to make sure you have a diversified portfolio.

Using mutual funds and ETFs to accomplish financial goals

Luckily, we have plenty of strategies and tools at our disposal when it comes to saving for short- and long-term goals.

One of the most important goals, for example, is having a fully stocked emergency fund. This helps through life's curveballs. Examples where an emergency fund is beneficial can be the deductible you'd have to pay if you got in a car accident or to cover the gap if you have an unexpected loss of employment. An emergency fund should be kept in an easily accessible savings account. You don’t want these funds tied up in a mutual fund or an ETF.

Mutual funds and ETFs can help with long-term financial goals like saving for retirement.

How do I decide between a mutual fund and an ETF?

It depends on your strategy.

Some investors use strategies like dollar cost averaging to invest frequently. This is the method of systematically investing shares regardless of price. This leads to purchasing more shares when prices decrease and less shares when prices increase. The goal is to help reduce the average cost of shares purchased over time and to develop a good habit of investing for the long haul.

Some investors might prefer mutual funds over ETFs because ETFs incur trading costs and require a market order for every purchase, whereas mutual funds can be automatic.

On the other hand, if the investor is tax sensitive, they might prefer an ETF index fund over an actively managed mutual fund.

These are just a few of the considerations potential investors take into account as they decide which option is best for their circumstances. Whether you're ready to seek further guidance from a financial advisor or get started yourself, USAA has a full range of options to help you find what works for you.