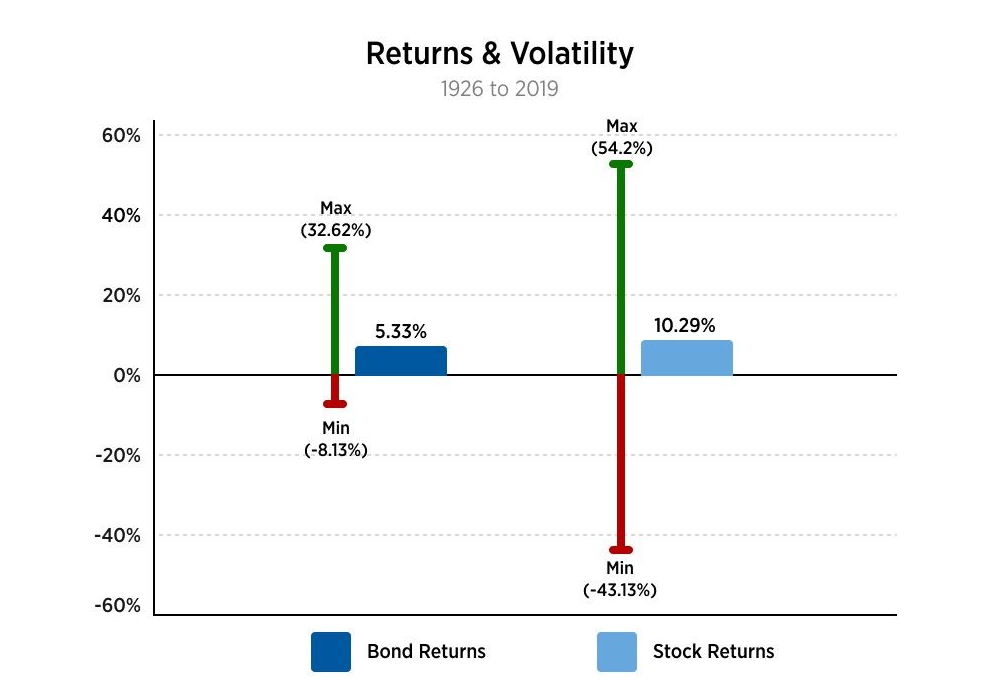

In that same study, the difference between the best year and the worst year of the 100% bonds portfolio was 40.75%. The same comparison for the 100% stocks portfolio was 97.33%. We also saw number of years with a loss increase from 14 for a 100% bond allocation to 26 for a 100% stock allocation. In short, while stocks experienced a greater return, it came with much more volatility and more years with negative returns. Thus, my roller coaster analogy.

How to pick your risk tolerance

Most financial advisors and investment tools use a risk tolerance questionnaire to help their clients select an appropriate risk tolerance. A series of questions helps determine appetite for risk and then gives a recommended portfolio based on those answers.

One good technique is to imagine a time when the market dropped significantly and for you to put yourself in that situation. Would you have been able to withstand a drop of that magnitude? It's much easier to do this if you actually lived through a market drop. What did you actually do? This can help you narrow down an appropriate risk tolerance.

A behavioral study by Tversky and Kahneman highlight the fact that most investors hate losses far more than they love gains — and that many investors overestimate the amount of risk they can emotionally handle. Having said that, there are also risks associated with being too conservative, such as failing to keep pace with inflation or running out of money in retirement.

But risk tolerance is only one consideration. You also need to determine whether your risk tolerance lines up with your risk capacity.

Risk tolerance versus risk capacity

Risk capacity measures a person's financial ability to take on risk. In general, investors with a longer investment time horizon have a higher risk capacity. They have a greater capacity for risk because they have time to recover if the markets fall. Someone who plans to retire in 30 years has much more time to wait for a market recovery than someone who plans to retire next year. But keep in mind that there's never a promise that the markets will recover. It's not a guarantee.

Here's another example where risk tolerance and risk capacity might not match. An investor may be very risk tolerant by nature. She seeks the thrill of starting her own business. She loves to go skydiving and rock climbing. If she invested according to her risk tolerance, she'd have lots of stocks and few bonds or cash in her portfolio.

Here's the kicker: This investor is in her 60s and plans to retire in a few years. Although by nature, she is willing to take on risk, she has a low risk capacity because she can't afford to take on risk like she could have in her 20s. If there were a market downturn, she'd stand to lose significantly, affecting her retirement lifestyle or even forcing her to work longer and delay retirement. She might not have enough time for the market to recover until she needs to begin accessing the funds.

On the flip side, if people invest too conservatively when they're young, they may not earn a return that outpaces inflation. This is another risk tolerance and risk capacity mismatch. They may be naturally risk adverse but have a huge capacity for risk as they don't need their funds for another 30 to 40 years.

What if I choose the wrong risk tolerance?

Investors typically discover they've chosen the wrong risk tolerance at one of two times: when the market drops, or when it rises quickly. Unfortunately, those are difficult times to make changes.

Here's why: If an investor sells some or all of their investments during a market low, they lock in a loss. It might be better to wait until the market recovers and then adjusting their risk tolerance at better prices.

On the other hand, if they see the market increasing and worry they're missing out because they invested conservatively, they might buy as the market is elevated.

It's important to remember throughout your investing journey that past performance is no guarantee of future results. Just because the market is decreasing doesn't mean it'll continue to decrease further. Also, just because the market is increasing doesn't mean it won't continue to go up.

How to right-size risk tolerance and risk capacity

Begin by answering the risk tolerance questions honestly. There's no reward for being super risk tolerant and there's no punishment for being super conservative. Also keep in mind the time horizon as that can help guide risk tolerance and risk capacity. If retirement funds aren't needed for another 30 years, this can help the investor be more comfortable assuming a level of risk that can help them achieve their goals.

Then, at least yearly, investors should reevaluate their risk tolerance and risk capacity. As we've shown, the passage of time and life circumstances likely affect both — and it's not advisable to make reactionary adjustments. If investors are unsure, it's a good idea to meet with a reputable financial advisor to determine the best time to make a change, if one is needed.