Source: myFico Opens in a New Window See note 1

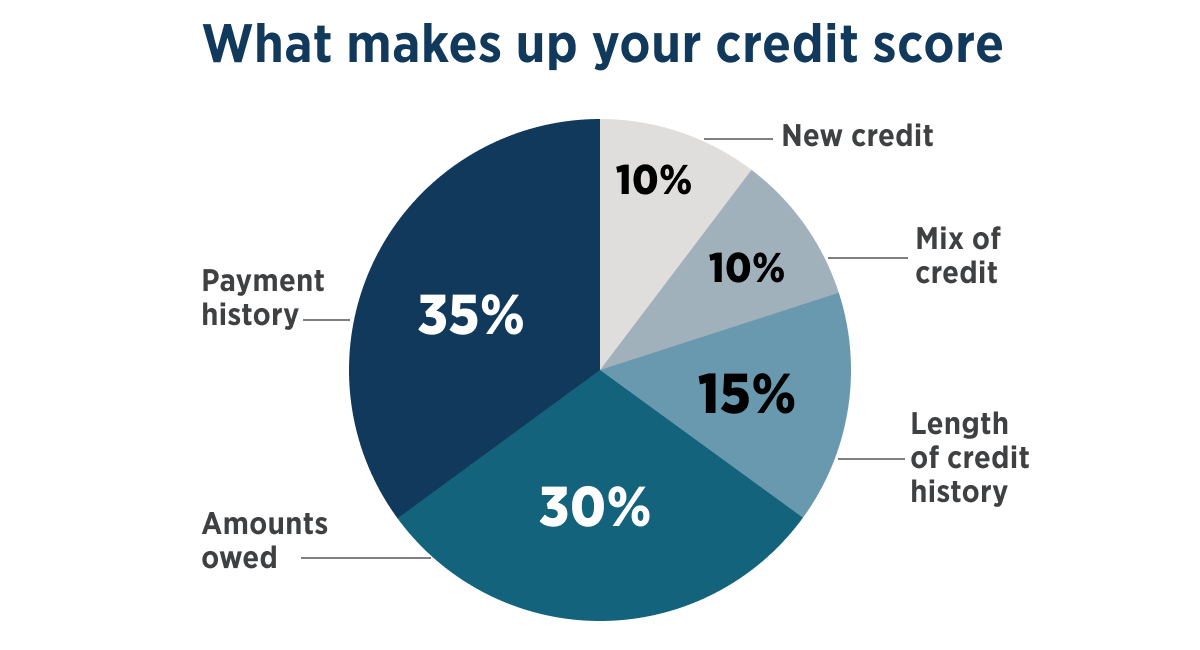

- Payment history (35%): Lenders want to know if you can make payments on time. After all, if you're late on one payment, there could be a greater chance you'll be late on another.

- Amounts owed (30%): Lenders want to be sure you aren't overextending yourself, so they're interested in how much you owe. How much is too much depends on your specific credit profile.

They consider several factors, including:

- The total amount you owe across all your accounts.

- The amount you owe on different types of accounts.

- The amount you owe versus the amount of credit available on revolving credit accounts. This is also known as utilization.

- The number of accounts with balances.

- How much you still owe on an installment loan compared to the original loan amount.

- Length of credit history (15%): The longer you've had credit, the better your credit score should be, if everything else is in order, of course. If you're newer to credit, take heart: You can still have a good credit score if you take care of business in the other four categories.

- Mix of credit (10%): In your wallet or filing cabinet, you probably have several types of credit: think credit cards, retail accounts, installment loans, mortgage loans and finance company accounts. FICO® says people without credit cards are often viewed as a higher risk than those who have credit cards and use them responsibly.

So how do you responsibly use a credit card?

- Always make payments on time.

- If possible, pay off your entire balance every billing cycle.

- Don't charge more than you can afford to repay.

- New credit (10%): When you open too many new accounts in a short time, lenders see you as a higher risk. This category considers how many new credit accounts you have.

That information is classified by several factors, including:

- The type of account.

- How many inquiries you have.

- The length of time since those inquiries were made.

- How long it's been since the last time you opened new credit.

- Whether you have good recent credit history.

Myth 2: My credit score will drop if I get credit counseling.

Fact: Credit counseling See note 1 Opens in a New Window doesn't negatively affect your score. This is important to understand because some people who could benefit from credit counseling are afraid to seek help. They worry it could send lenders the wrong message.

Myth 3: When I check my credit score, it should match the score the lender gave me.

Fact: You don't have a credit score, you have credit scores. Accessing one universally agreed-upon credit score would make life easier, but that's just not the case, not even close.

FICO®, the most common household name for credit scores, is a data analytics company that's developed credit score models based on information in your credit reports. And yes, there are more than one of those as well. You have an Experian FICO® credit score based on information in your Experian® credit report, an Equifax FICO® credit score based on that information and a Transunion FICO® credit score based on that report.

If only it stopped there.

FICO® has many models. For example, there's FICO® Score 9 and FICO® Score 8, and a version of each based on information from each credit report. And then there are scores specific to auto, credit cards and mortgages based on information from each of the three credit reporting agencies. And just think, we haven't even touched on the other credit scores beyond FICO®, like VantageScore®, which also has multiple versions.

Lenders can choose product-specific scoring models, such as FICO® Auto Score for an auto loan because there's different risk involved in lending money for different products. They might also pull your credit information from a different credit reporting bureau from the one you checked.

So, is there one particular credit score that matters? No. Here's what does: The story your credit report tells. The score is simply a numbered reflection of what's in your report. If you're declined for a loan or receive an interest rate less favorable than expected because of your credit, focus on the information in your report.

Myth 4: Checking my own credit will hurt my credit score.

Fact: Checking your own credit creates an inquiry on your credit report, but not all inquiries impact your credit score.

There are two types of inquiries: "hard" inquiries related to a credit application and "soft" inquiries from looking at your own credit report. Hard inquiries influence your score, but soft inquiries don't. Learn more about hard and soft inquiries Opens in a New Window. See note 1

At least once per year, review all three of your credit reports: Experian®, Equifax® and Transunion®. You can visit the Annual Credit Report site to get these reports for free Opens in a New Window. See note 1

When you review your credit report, look for:

- Incorrect information, which is more common than you might think and should be disputed immediately.

- Late payments and collections, which can really hurt your score.

- Utilization, which is the amount you owe versus the amount of available credit. The higher your utilization, the lower your score.

Past mistakes don't have to haunt you forever. If you focus on what you can control and improve going forward, your score will follow over time.

Myth 5: A higher credit score means you have more debt.

Fact: Credit score models consider the different types of credit you have, from credit cards and auto loans to your mortgage. However, these models don't reward owing more money. In fact, the second largest factor in the FICO® credit score model is the amount you owe. The less you owe, the better.

Myth 6: Getting married affects your credit score.

Fact: That's not necessarily true. You don't share a credit score with your spouse when you get married, and you'll continue to maintain separate credit information. However, if you open any joint credit accounts, they'll appear on both of your credit reports. This is where your spouse's credit history can impact you.

Let's say you and your spouse decide to apply for a joint credit card or a home loan. If one of you has bad credit, it could impact your qualification and interest rate, as the lender might not just look to the highest credit score between spouses when making the determination.

Myth 7: Closing a credit account will improve my credit score.

Fact: Closing an account doesn't immediately remove it from your credit report and could have the opposite effect. Negative history can remain up to seven years, and positive history remains for 10 years from the last date of activity.

Because utilization, the amount of credit you have available versus the amount of debt you owe, is one of the biggest factors that impacts your credit, if you close a credit account, you lose the available credit limit on that account. That increases your utilization and could lower your credit score.

If you plan to apply for new credit in the next three to six months, you might want to wait before closing an account.

Myth 8: Credit scores consider income and demographics.

Fact: While lenders may consider your income in relation to the amount of debt you owe, income isn't included in your credit report and has no impact on your credit score. Neither does demographic information such as race, origin, religion, profession, disabilities, sexual orientation and military status.

Myth 9: Employers can check your credit score before offering you a job.

Fact: Some employers can check your credit history as part of the hiring process. However, they don't have access to your credit score.

Often, employers in the financial services industry or the military check potential employees' credit history. Why? According to them, it's helpful to know how responsible and financially stable you are.

Myth 10: I can improve my credit score by carrying a balance on my credit card.

Fact: While you do need to demonstrate that you can properly use credit cards, which means actually using them, you don't need to carry a balance from month to month, all the while paying unnecessary interest to the card issuer.

When your billing cycle ends for the month, any outstanding balance is reported to the credit bureaus, which shows usage. Paying off that balance in full and on time before the bill is due will not only save you money, but it will also be reflected in the two biggest factors of your credit report — payment history and the amount you owe.