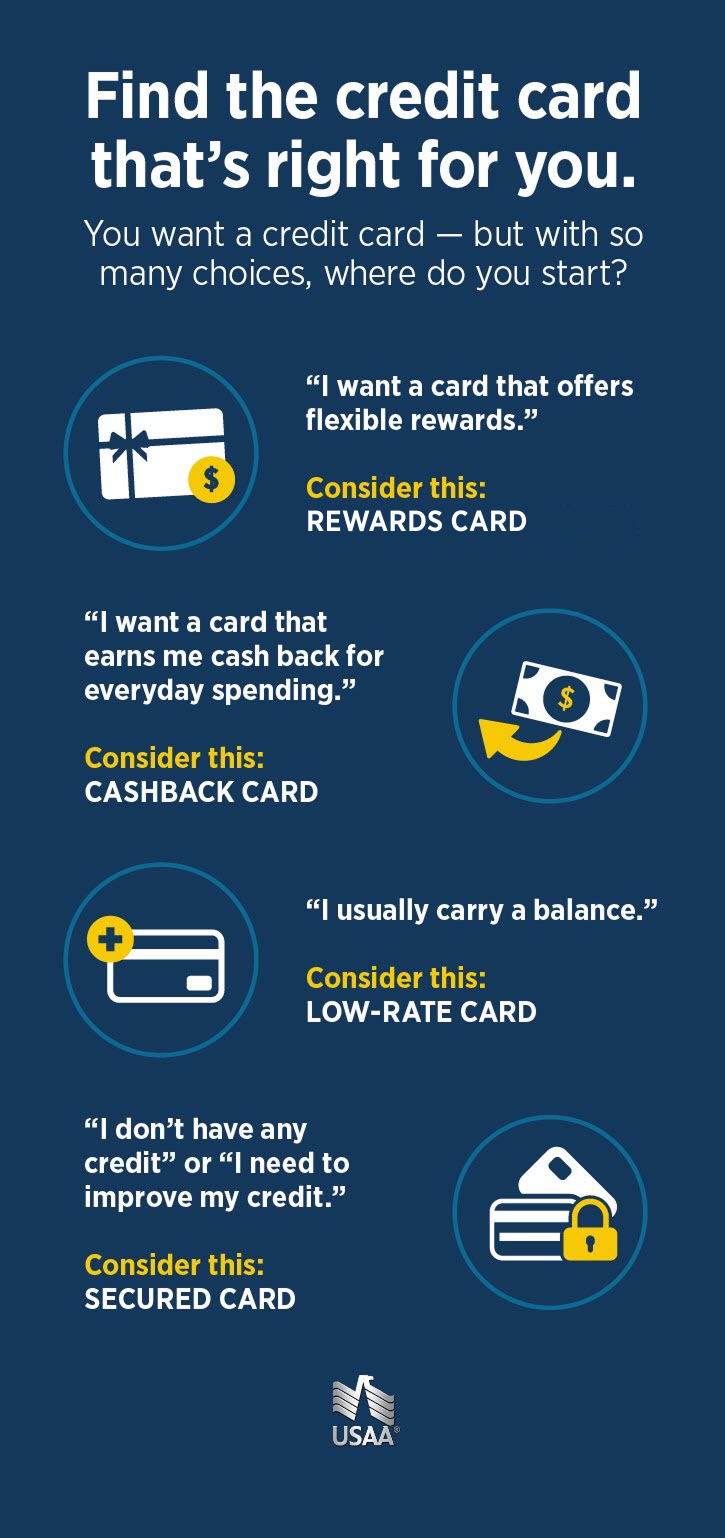

Option 1: Rewards card

With a rewards card, you get points based on your spending habits. Different cards may offer more points for purchases in one category over another. For example, one might give you double points on gas and dining out, while another might give you double points on travel. In either case, rewards would apply to qualifying purchases only. So, choose a card that matches your spending habits to maximize your rewards. You can typically redeem points for travel, cash back, gift cards and more.

Is a rewards card right for me?

The interest rate on rewards cards may range, in percentage terms, from the teens into the 30s, and the company issuing the card may charge an annual fee. These are generally best suited for people who pay off their balance in full each month and receive more value from the rewards than any rates or fees that may be associated with the card.

Option 2: Cashback card

A cashback card is like a rewards card, but instead of accumulating rewards points, you earn cash back with each purchase. Just like with a rewards card, cash back would apply to qualifying purchases only, so it's important to choose a card that matches your spending habits. Read the fine print first, because some cards pay the same cash back rate regardless of where you spend or what you buy. Others vary or may even have a cap on how much cash back you can earn.

Is a cashback card right for me?

Also like a rewards card, the APR for cashback cards tends to be higher and there may be fees associated. That means cashback cards are generally more suitable for someone who pays off or keeps low balances from month to month. Cashback and rewards cards tend to cater to those with a track record of positive credit usage.

Option 3: Low-rate card

A low-rate card doesn't accumulate rewards or cash back. Instead, it typically has a lower APR that varies depending on your credit profile and other factors. Also, most low-rate cards have no annual fees. When you're shopping around, be sure to compare details such as introductory APRs and how long those rates last.

Is a low-rate card right for me?

When card owners carry a balance from month to month, they pay more in interest. If that sounds like you, a low-rate card may be your best bet, so that the amount you pay in interest isn't as high as it typically is with a cashback or rewards card. You may also want to consider some ways to pay off your current credit card debt.

Option 4: Secured credit card

Secured credit cards offer a spending limit based on a deposit you place with the card issuer and your creditworthiness. For example, you might deposit $500 with the bank as security in exchange for a credit card with a $500 credit limit. Each month when you make your payments, the card issuer will report the information to the credit bureaus. So, paying on time, every time, could help you establish a good track record. This type of card may or may not offer rewards.

Is a secured card right for me?

Secured credit cards are typically a great option for people who want to establish credit for the first time or are hoping to rebuild their credit score. Maybe you're a parent who wants to help your young-adult child build their credit. Or maybe you've had a difficult credit history and want to improve your own standing. Either way, secured credit cards help you get in the game and an added benefit, if managed correctly, could be an improved credit score.

Credit card offers to meet your needs

Some cards may seem great when you read the promotional copy. But avoid the temptation to apply without taking a close look at the details. It's important to apply for a card that matches your spending habits and how you manage repayments. If you're not a detail-oriented person, you probably don't want a card with a promotional rate that will change after a period of time, leaving you with a high APR that catches you by surprise.

And a card that offers 1.5% cash back or attractive rewards but charges a 30% interest rate? It isn't as good of a deal as earning no cash back with a much lower 15% interest rate if you don't pay your balance in full before interest is charged each month, no matter how tempting the cash back or miles may sound.

In addition to the APR and the type of rewards, you'll want to consider any fees associated with the card, promotional rates, penalties for missed or late payments, and any other terms and conditions. If you're currently using a high interest rate card, you may want to look into a balance transfer.

Along with the fees and penalties, be sure to compare the benefits such as extended warranties, price protection or travel protection associated with the cards you're considering. Some credit cards carry a foreign transaction fee, which is an important consideration for military members who are deployed or stationed overseas.

At the end of the day, managing your credit card usage in a responsible manner can help set you on the path to financial security, while building your credit.