For many Americans who have a less-than-stellar credit history or no credit history at all, credit can be a source of ongoing frustration.

That's partly because credit cards have become such an important player in our financial lives. Whether we're shopping online, using an app-based ride service or visiting a store that doesn't take cash, not having a credit card can be a hassle.

Of course, a debit card can be an option in these situations, but they don't always offer the same features and protections. So if your history of credit usage, or lack thereof, has left you without a card, are all of these modern conveniences out of your reach?

The short answer is no. Read on to learn how you can build credit and improve your chances of being approved for a credit card.

What a 'good credit score' really means

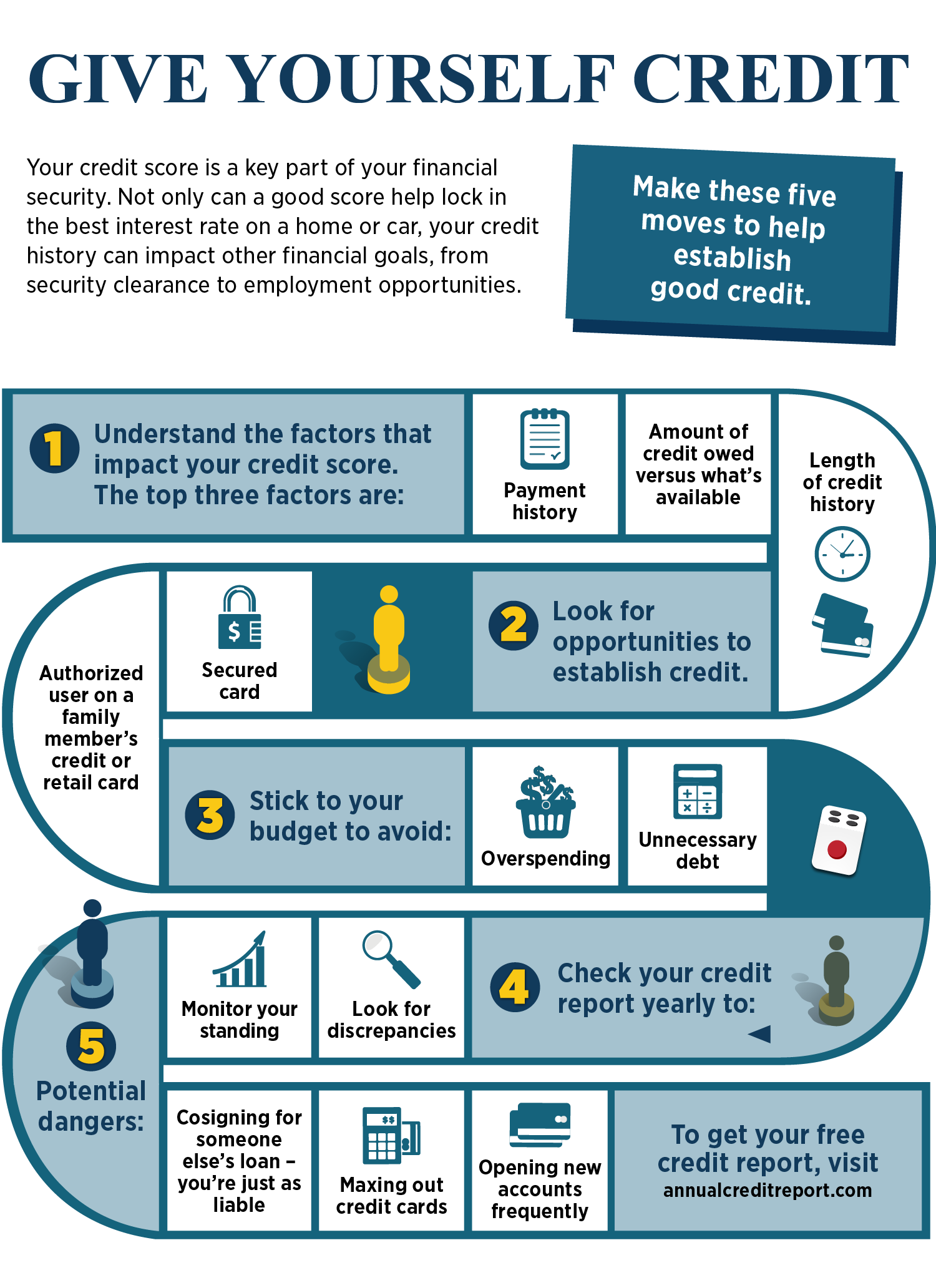

First off, what's a good credit score and is it required to get a credit card?

A good credit score can mean different things to different people. There's no firm rule that defines a good credit score, as it often varies by the credit card issuer and the credit card itself.

These behaviors, however, affect your credit score because they're important to lenders who determine whether to approve your credit card application.

- You make routine, on-time payments.

- You don't max out credit limits or owe a significant portion of your total available credit. Ideally, you pay off your credit card balances in full each month.

- You have a long credit history.

- Your accounts don't fall into collections.

A common, yet false, assumption is that if you ignore a credit problem for long enough or close an account that's giving you trouble, it'll go away. This couldn't be further from the truth. Bad credit history can stay on your credit report for up to seven years, and certain types of bankruptcy for up to 10 years. Late payments and bankruptcies will have a negative impact on your credit the entire period they are on your report, but the degree of impact typically lessens over time.

Improve your credit score by paying down debt.

It may sound simple, but if paying off debt were easy, fewer Americans would struggle with it.

Paying off debt starts with managing your spending. To do this, make a budget to be sure you spend less than you earn, and stick to it. Factor in on-time payments for any remaining open credit accounts.

We suggest the "Three A's" approach to getting debt under control: assess, avoid, attack.

Assess

Check your credit to understand what you owe and where. You can check your credit report once a year for free at annualcreditreport.com Opens in a New Window. Look at your statements and make sure you recognize everything listed. If you see any mistakes, dispute them. Take a look at your current spending as well.

Avoid

Until things are under control, try to avoid using credit. Build some cushion into your savings so you don't have to use credit if something unexpected happens. The industry norm is to have three to six months of living expenses saved up in an emergency fund savings account.

But, don’t let that amount discourage you. Start with a $1,000 goal. That's a car insurance deductible, maintenance around the house or a medical bill payment. Then, continue saving until your emergency fund is fully funded.

One way to get there is through a concept called "step-up savings." Here's how it works: Over a 52-week period, save $1 more per week than the previous week. For example, save $1 the first week, $2 the second week, $3 the third week, and so on. At the end, you'll have $1,378.

Attack

For the debts you have already, get those balances in order. There are two schools of thought when it comes to this. Either pay off the smallest balance first or pay off the one with the highest interest rate first. In either case, you pay the minimum on all but one debt. For that one debt, you'll pay extra until it's paid off. Then you'll roll that payment amount onto the next debt and so forth.